Vermont Association of Broadcasters

Vermont Association of Broadcasters

Vermont Radio & TV Station leaders,

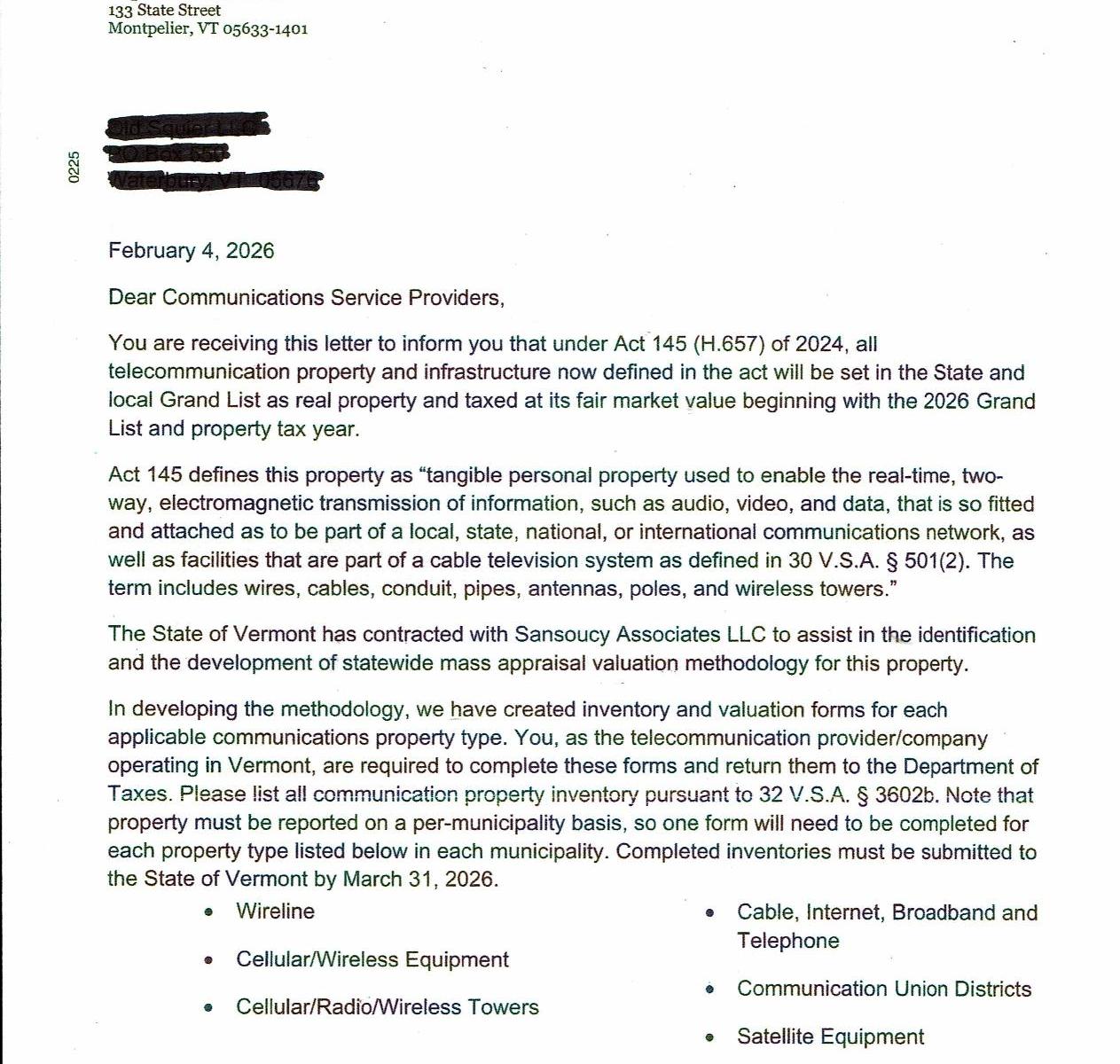

It was brought to the VAB’s attention on Friday, February 13th that some stations had received a letter in the mail from the Vermont Department of Taxes informing them of a new state tax on telecom property passed in Act 145 that their station is supposedly subject to.

If you too received a letter like this, please let me know by forwarding it to me at wendy@vermontbroadcasters.org

Part of the VAB’s mission is to support and advocate for broadcast station’s best interests, so the VAB is commited to fighting this on your behalf. Not only did I follow last year’s telecom tax bill (H.657) that became Act 145, the legislation referred to in the letter, but I have since reviewed all 14 pages again and have determined the following:

- Section 1 of Act 145 defines “telecommunications service” as well as who is included and neither broadcast radio or television fit the statute’s definition or list of inclusions. Broadcast radio and broadcast television signals are not “interactive” and do not “pass through the public switched network.”

- Section 10 of Act 145 defines “communications property” as “tangible personal property used to enable the real-time, two-way, electromagnetic transmission of information, such as audio, video, and data, that is so fitted and attached as to be part of a local, state, national, or international communications network, as well as facilities that are part of a cable television system as defined in 30 V.S.A. § 501(2). The term includes wires, cables, conduit, pipes, antennas, poles, and wireless towers.” The broadcast of radio and television signals is not two-way and is not a part of any communications network.

- The word “wireless towers” is used one time in the bill/act statute, but the department of taxes changed the phrase to “phone/radio/wireless towers” as they developed the website and inventory form referenced in the letter.

- The intent of this bill/act is to create a tax to pay for state phone (ie 911) and broadband expansion projects and the tax is only intended for telecommunications services and cable television who are able to pass the tax on to their customers/subscribers. Broadcast radio and broadcast television have no customers/subscribers to pass the tax on to.

The VAB has hired an attorney to assist in crafting an effective argument and guide us through whatever needs to be done to get the VT Department of Taxes to course-correct. But it starts with understanding which broadcast stations have received this letter. So if you get it, please reach out to the VAB as soon as possible.